This guide will cover the difference between wholesale versus retail lending. We will discuss the pros and cons of wholesale versus retail lending for consumers and loan officers. Do you need clarity about the difference between wholesale versus retail lending? Which one is your solution and best option for your financial needs? Dale Elenteny explains the benefits of wholesale lending as follows:

The benefits of wholesale lending include access to capital at a lower cost, flexibility in loan terms, and a quicker turnaround time. The risks of wholesale lending include higher default rates and the possibility of being taken advantage of by unscrupulous lenders.

Whether approaching the real estate market as a borrower or a lender, understanding these two types of lending can make all the difference in your financial success. In this blog post, we will valiantly explore what makes wholesale versus retail lending unique, their main advantages and disadvantages, and how to determine which is right for you. So please take a few moments and dive into the lending world!

Introduction to Wholesale Versus Retail Lending

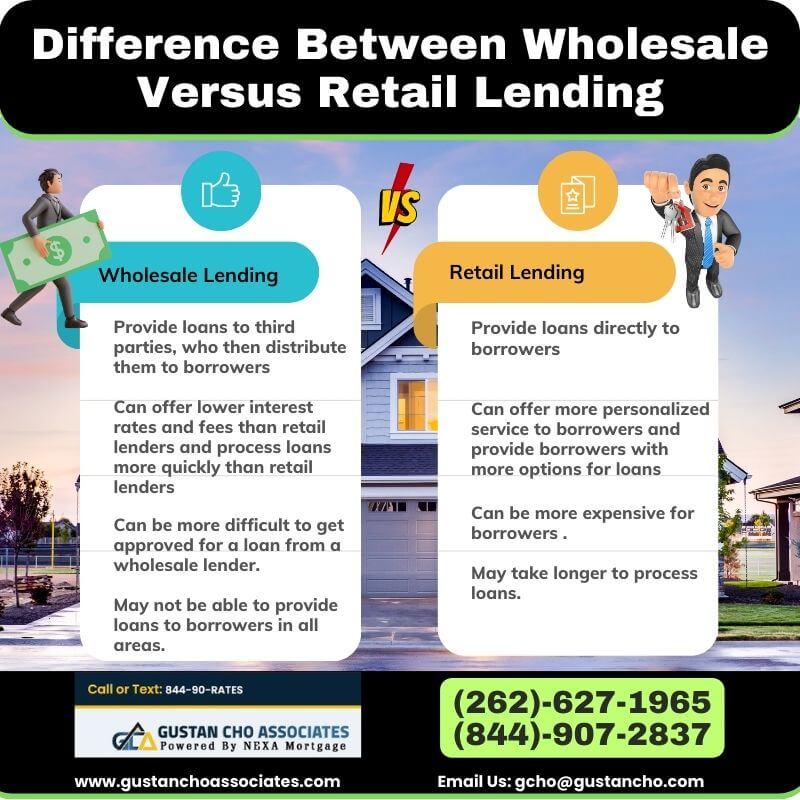

Wholesale versus retail lending is two distinct types of lending that serve different purposes. Banks and other financial institutions typically use wholesale lending to finance the purchase of large items, such as non-conforming or non-traditional loans for real estate or vehicles. On the other hand, retail lending is when mortgage bankers fund their loans, whether real estate or smaller loans, such as those used for personal expenses. John Strange of Gustan Cho Associates explains the difference between wholesale versus retail lending as follows:

The main difference between wholesale versus retail lending is the loan size. Wholesale loans are typically much more extensive than retail loans. Wholesale loans come with a higher risk for the lender and a higher potential return. Retail loans are typically smaller and have a lower risk for the lender.

Another critical difference between wholesale versus retail lending is the interest rate. Wholesale lenders charge a higher interest rate because they assume a higher level of risk. Retail lenders charge a lower interest rate because of lower risk. Your needs and objectives depend on which lending service is right for you. If you need a larger loan for a significant purchase, then wholesale lending may be the best option. Retail lending may be better if you need a smaller loan for personal expenses.

Benefits and Risks of Wholesale Versus Retail Lending

Wholesale lending is loaning money to a business or individual through a third-party lender, such as a bank or private equity firm. The borrower then uses the funds for their intended purpose, such as purchasing inventory or real estate. Wholesale lenders may offer a wider range of loan products and better interest rates but require greater creditworthiness from the borrower.

The main benefit of wholesale lending is that it offers lower interest rates than retail lending. This is because wholesale lenders are not subject to the same regulations as retail lenders and can offer more competitive rates. Additionally, wholesale lenders typically have more flexible repayment terms than retail lenders.

There are also some important risks to consider associated with wholesale lending. For instance, if the borrower/buyer defaults on their loan, the lender may have difficulty recouping their losses. Also, wholesale lenders may be less likely to work with borrowers with poor credit histories. Wholesale lending is lending money to businesses or individuals through a third-party lender, typically at a lower interest rate than what is offered by retail lenders.

How Does Wholesale Lending Work?

Wholesale lending provides borrowers loans through a third-party broker or other intermediary. The benefits of wholesale lending include access to a larger pool of potential borrowers and the ability to negotiate better terms and rates. Alex Carlucci, a top-producing loan originator, and mortgage broker, shares his concerns about risks associated with wholesale lending:

There are also some valid concerns associated with wholesale lending, including the potential for fraud and abuse by brokers and intermediaries. A third-party lender extends credit to a borrower as part of wholesale lending.

The intermediary lender then sells the loan to another financial institution, such as a local or national bank or an insurance company. This type of lending has many benefits, including the possibility of lower interest rates and lower fees. The borrower/buyer may default on the loan, or the loan may not be sold to another institution, posing a risk.

Benefits and Risks of Retail Lending

Retail lending is the process of providing loans to individuals rather than businesses. The main benefit of retail lending is that it allows lenders to tap into a new market and expand their customer base. However, some risks are associated with retail lending, including higher default rates and more volatile interest rates. Angie Torres oversees the secondary mortgage markets at Gustan Cho Associates. Angies explains what retail lending as follows:

Retail lending is providing loans directly to consumers rather than through third-party institutions. This type of lending has several common benefits, including the ability to offer more personalized service and better terms. However, retail lending also comes with a few risks, such as the potential for higher default rates.

Default rates on retail loans are generally higher than those on commercial loans because individuals are more likely to experience financial difficulties than businesses. If you’re unsure which type of lender is right for you, it’s always best to speak with multiple providers to compare your options and find the best fit.

Is It Better To Work With a Mortgage Broker or Retail Lender?

Retail lending is often more sensitive to changes in interest rates than commercial lending, meaning lenders may have to adjust their pricing more frequently to say competitive. In general, retail lending has higher rates versus dealing with a mortgage broker with wholesale lenders, advises John Strange of Gustan Cho Associates:

Ultimately, which type of lender is right for you will depend on your credit score, preferred loan product, and financial goals. Consider all the factors carefully before deciding so that you can get the best deal possible.

When choosing between wholesale versus retail lending, weighing the pros and cons of each option is important. For some borrowers, retail lending may be the best choice. Others may find that wholesale lending is a better fit for their needs. Ultimately, the decision comes down to what’s most important to the borrower regarding cost, convenience, and risk.

Steps to Finding a Wholesale Lender

If you’re looking for a wholesale lender, you must take some steps first. The first thing to consider is deciding the property type you want to purchase. Wholesale lenders typically lend on properties that need to be repaired or renovated. Since the property will likely be sold at a discount or reduced price, you should be aware of the repairs needed before you submit your offer to make the most of it.

To locate wholesale lenders in your area, you need to determine and locate the type of property that interests you. You can find this information at various places online, or you can ask your real estate agent for recommendations. Once you have a list of potential lender candidates, it’s time to shop for the best rates and terms.

It would be best to remember some vital things when comparing wholesale lenders. First, consider each loan’s interest rate, fees, and costs. You should also ensure that the lender is willing to be flexible and work with you on the loan terms. Some wholesale lenders, for example, require a larger down payment than typically required when financing through a retail lender.

Steps to Finding the Right Lender With Lowest Rates

A few key steps can guide you when looking for the right lender, whether you’re going the wholesale or retail route. Know your credit score and history. This will give you a good starting and leverage point for finding lenders that work with borrowers in your credit range. Mike Gracz, a loan officer at Gustan Cho Associates, advises borrowers to shop for the best rates:

Research different types of loans and lenders. You’ll want to compare rates, terms, fees, and other factors to find the best deal. Consider your financial goals and needs. Make sure the loan works with your long-term plans. Shop around and compare offers from multiple lenders.

Don’t just go with the first initial offer you receive – be sure to compare and contrast to get the best deal possible. Read the fine print carefully before you sign anything. You want to avoid getting stuck with hidden fees or unfair terms. You can shop for the lowest rates with bad credit. Not all bad credit lenders have the same rates.

Tips for Borrowers Choosing Between Wholesale Versus Retail Lending

There are important factors that borrowers should consider when choosing between wholesale versus retail lending. Wholesale lenders typically have more flexible underwriting standards than retail lenders. This means that borrowers with less-than-perfect credit may be able to get qualified for a loan from a wholesale lender that they would not be able to get from a retail lender.

Institutional investors, such as banks or hedge funds, typically fund wholesale loans. Retail loans, on the other hand, are typically funded by individual investors. This can make quite a difference in the terms of the loan. For example, wholesale loans may have lower interest rates and longer repayment terms than retail loans.

Third, borrowers should consider the fees associated with each type of loan. Wholesale lenders typically charge higher origination fees than retail lenders. However, lower interest rates and closing costs often offset these higher fees. Borrowers should compare all of these factors before choosing a loan type.

Is a Mortgage Broker the same as a Wholesale Lender?

As a potential homebuyer, you may have encountered the terms “mortgage broker” and “wholesale lender” and wondered if they are the same. The short answer is no; they are not – there are some key differences between the two. A mortgage broker is a middleman who works with borrowers and lenders to secure financing for a home purchase. On the other hand, a wholesale lender is a direct lender that provides funding for loans originated by mortgage brokers.

One of the main and important advantages of working with a knowledgeable mortgage broker is that they have access to many different lenders. The wide array of lender choices allows them to shop around for their clients’ lowest, best rates and terms.

On the other hand, wholesale lenders only offer their products and rates. Another difference is that the lender typically pays mortgage brokers a commission, while wholesale lenders do not charge borrowers fees. You may get a better overall deal by working with a mortgage broker than going directly to a wholesale lender.

Is It Better To Work With Wholesale Versus Retail Lending

When it comes to finding a great mortgage broker, there are some things you should keep in mind. First, you should ensure the broker is licensed and has a good reputation. You can search and check with the Better Business Bureau or your state’s banking department to see if common complaints or issues have been filed against the broker: Ethel Matthews, a dually licensed realtor and loan officer at GCA Mortgage Group, Inc., advises the following when it comes to finding the best mortgage broker with the best rates and a lot of mortgage options:

You should ask around for referrals from people you trust. If you know someone from your close circle who has recently bought a home, they may be able to recommend a good mortgage broker.

You should shop around and get quotes from several brokers before deciding. This will help you ensure that you’re getting the best deal possible. It also helps if the broker has several, maybe even 100’s different lenders to choose from. Ensure you understand all the fees associated with the loan before signing anything. This way, there won’t be any surprises down the road.

Working With a Mortgage Broker Versus Mortgage Banker

Wholesale versus retail lending is two different methods of lending money. Retail lenders provide more personalized services, have their loan products, and cater to individual borrowers. If you should decide to buy, before you begin looking for a home and during the process, we have vast experience working with buyers to get them ready to purchase their dream home. We can take you through your home loan’s buying and financing process. We also can connect you to title companies/attorneys and real estate agents in your area that can help as needed.

After you’ve found a few wholesale lenders you’re comfortable with, submit your loan application. Be sure to include all required information and documentation, such as financial statements and proof of income. Once your application has been approved, you can begin the process.

If you have questions on the content of this guide regarding mortgage brokers versus mortgage bankers, please call or text Ronda Butts at 407-460-7999 or email at ronda@gustancho.com for more information and further assistance. Ronda is an experienced referral agent, a dually licensed real estate agent, and a mortgage originator. Ronda has successfully guided many homeowners through obtaining a home on both the lending and real estate side. Ronda Butts does not represent buyers or sellers but offers free consultation in 48 states at Gustan Cho Associates by connecting homeowners, buyers, and sellers to the needed sources.