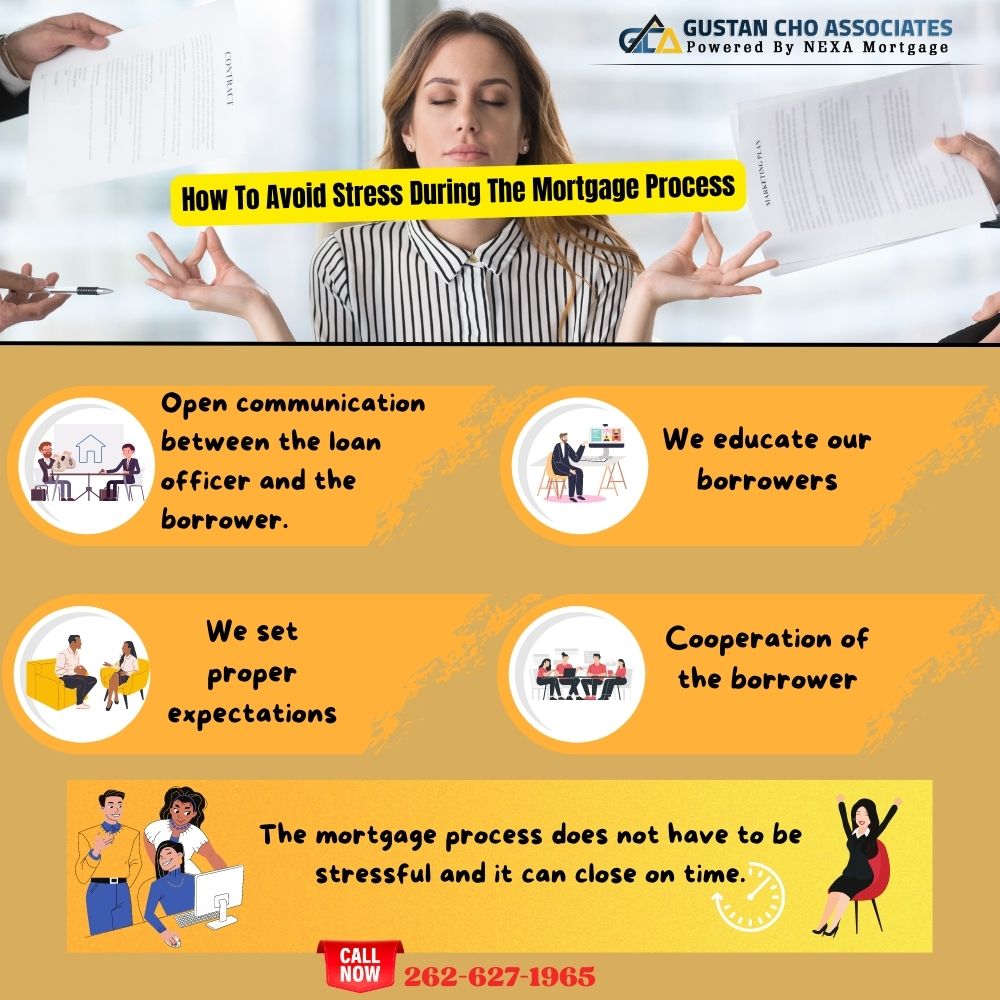

In this guide, we will cover how to avoid stress during the mortgage process. The mortgage process does not need to be stressful. Open communication between the loan officer and the borrower. The first reason there is stress during the mortgage process is that the documents required were submitted with paperwork missing. Gustan Cho of Gustan Cho Associates said the following about stress during the mortgage process:

It is the responsibility of the mortgage loan officer and mortgage processor to make sure there is no stress during the mortgage process. Borrowers ofter stress during the mortgage process because the loan officer did not properly issue a pre-approval letter.

The stress during the mortgage process is that the documents required were submitted with paperwork missing or parts of docs were not legible. It is better to take a few steps backward to go forward and ensure all documents required are legible with no missing pages. In the following paragraphs, we will cover why borrowers stress during the mortgage process and ways on avoiding it. We will discuss the most common reasons for stress during the mortgage process.

How To Avoid Stress During The Mortgage Process

Over 80% of our borrowers at Gustan Cho Associates could not qualify at other lenders due to a last-minute mortgage loan denial due to lender overlays.

Many of our borrowers at Gustan Cho Associates are folks who transferred their mortgage loans from other lenders due to stress during the mortgage process or because of the lender having overlays.

Many borrowers are frustrated homebuyers and meet the mortgage guidelines. However, something happened either due to a lack of communication or the loan officer not realizing the lender had lender overlays.

Submitting Incomplete Documents To Underwriting

People buying a home for the first time feel overwhelmed by the number of mortgage documents required for the home loan process when applying for a mortgage. It seems like there’s an endless demand for documentation needed and documents required for the mortgage process.

The mortgage process is an actual process. It takes the lender and the borrowers to work as a team for the mortgage process to go smoothly. The mortgage loan process cannot be rushed.

One of the most common reasons for stress during the mortgage process is due to the loan officer issuing a hasty pre-approval without carefully combing over each required document to process the mortgage loan. In the following paragraphs, we will cover the documents required to start processing the mortgage loan application through the mortgage approval and closing process without any stress and delays.

The Start of The Mortgage Process

Once you get a pre-approval letter issued from your loan officer, you can start shopping for a house. Once you have signed a real estate purchase contract, the second step of the mortgage loan process officially starts. A mortgage processor gets assigned to you. The processor will request updated documents so they can prepare the file for a mortgage underwriter.

Keep in mind to begin any mortgage process have the following Documents Required to start the mortgage process. The initial start of the mortgage process is for the mortgage processor to gather all the documents required for the mortgage underwriter. The mortgage underwriter will kick the file back if she finds any documents not legible or pages missing. Once a files gets suspended by the mortgage underwriter due to missing pages or docs, the file gets kicked back to the mortgage processor and gets assigned back in the line.

A great mortgage processor will be knit picky to make sure the documents required for the underwriter are complete, legible, and updated to avoid the underwriting rejecting the file for updated conditions.

Credit Disputes Halts Mortgage Process

One of the biggest reasons for a last-minute mortgage loan denial is due to the loan officer and mortgage processor overlooking credit disputes prior to submitting the mortgage loan to underwriting. Overlooking credit disputes on non-exempt credit tradelines is the most competent thing any loan officer or mortgage processor can do.

You cannot have credit disputes during the mortgage process on non-medical collections, charge-off accounts, late payments, and any derogatory credit tradelines that is newer than 24 months old.

Medical collections are exempt. And so are non-medical collections with zero credit balance. Also, non-medical collection accounts that total less than $1,000 in outstanding collection balance are exempt from retraction. Older derogatory credit tradelines that are older than 24 months old are exempt from credit disputes being removed. Each lender has lender overlays on credit disputes. Lenders may require exempt credit disputes to be removed. All credit disputes that are not exempt need to be removed for the loan process to proceed.

How Removing Credit Disputes Cause Stress During The Mortgage Process

Removing credit disputes will drop credit scores when borrowers can no longer qualify. When a consumer disputes a derogatory credit tradeline, the credit bureaus will automatically discount the negative credit tradelines from the credit scoring model.

The verbiage consumer disputes this credit tradeline: Tradeline under investigation triggers an increase in credit scores because the credit bureau algorithm discounts the disputed credit tradelines like it does not exist. Therefore, there will be an increase in credit score.

When you remove the credit disputes, the derogatory credit tradeline will report like a freshly new derogatory credit tradeline so it will drop the borrower’s credit scores even more than before. There are many instances where the borrower no longer will qualify for a mortgage. The team at Gustan Cho Associates are experts in helping borrowers who got a last-minute mortgage loan denial due to loan officer mistakes. We have creative ways of getting you qualified and getting you pre-approved when other lenders cannot.

Best Mortgage Lender For a Stress-Free Mortgage Loan Process

Not all lenders have the same lending requirements on FHA, VA, USDA, and conventional loans. Not all lenders offer alternative mortgage options such as non-QM loans, bank statement mortgages, no-doc loans, fix and flip mortgage options, and other loan programs.

Gustan Cho Associates empowered by NEXA Mortgage, LLC are mortgage brokers licensed in 48 states including Washington, DC, Puerto Rico, and the U.S. Virgin Islands. We have a lending network of over 210 wholesale lending partners.

Per HUD agency guidelines, the minimum credit score requirement to qualify for an FHA loan is 500 FICO with a 10% down payment. To qualify for an FHA loan with a 3.5% down payment, you need at least a 580 credit score. However, most lenders will require a 620 to 640 credit score.

What Are Lender Overlays?

Why is it that one lender will approve an FHA loan with a 580 and a different lender will require a 620 FICO? Mortgage lenders can have higher lending standards that are higher than HUD’s minimum guidelines. These higher lending standards are called lender overlays. Not all lenders have the same mortgage rates on government and conventional loans. Some lenders will have substantially higher rates than others. This is why it is very important to shop and compare rates and terms when shopping for a mortgage.

Mortgage Loan Options

Here are the loan programs offered at Gustan Cho Associates:

- FHA loans

- VA loans

- USDA loans

- Conventional loans

- Jumbo mortgages

- NON-QM loans

- Non-QM jumbo mortgages with credit scores down to 500 FICO

- FHA 203k loans

- Reverse mortgages

- 90% LTV Non-QM Jumbo Loans

- Asset Depletion Mortgages

- No-doc home loans

- Fix and Flip Mortgages

- Doctors mortgage loans

- All-in-one mortgage

- DSCR Mortgages with no income documentation required

Gustan Cho Associates has a national five-star reputation for being able to do loans other lenders cannot due to its no overlays. Borrowers have many options when choosing a mortgage loan program that may best suit their needs. However, the common denominator for any loan process to run smoothly is to make sure the mortgage documents required are legible, complete, and turned in timely. Not having neat, legible, complete mortgage documents with missing pages is one of the main reasons for a loan denial, delays in the loan process, and stress.